The Wheel Strategy.

Real numbers. Honest take.

A beginner explanation of how the options wheel strategy works, what $302k in net premium collected actually means, and why the full picture is always more complicated than the screenshot.

What is the wheel strategy?

The wheel strategy is one of the more straightforward options strategies out there, and it is a good starting point if you are a stock investor curious about options. The core idea is simple: you sell options on stocks you actually want to own, collect premium, and repeat the cycle. It is called the wheel because it keeps spinning.

You do not need to be a finance professional to run this. You need a brokerage account that supports options trading, enough capital to back your positions, and a clear view of which stocks you are comfortable owning if things go against you. I use IBKR (Interactive Brokers), which is accessible to retail investors in Singapore and most parts of the world.

Sell a cash-secured put (CSP).

You sell a put option on a stock you are happy to buy. The buyer of that put is paying you for the right to sell you their shares at a fixed price, called the strike price, before expiry. You collect that payment upfront. It is yours to keep regardless of what happens next.

Two possible outcomes:

Stock stays above your strike price at expiry. The put expires worthless. You keep the full premium and go again.

Stock drops below your strike price. You get assigned. You now own 100 shares at your strike price. But your effective cost is already lower because you collected premium upfront.

The key thing to understand here: you should only sell puts on stocks you genuinely want to own at that price. If the stock drops hard and you would not want to hold it anyway, this strategy will hurt you. Stock selection matters more than the options mechanics.

Sell a covered call.

Now you own the shares from assignment. You sell a call option against them. Someone pays you for the right to buy your shares at a fixed price. You collect more premium.

Two outcomes again:

Stock stays below your call strike. The call expires worthless. You keep the premium and sell another call next cycle.

Stock rises above your call strike. Your shares get called away. You sell them at the strike price, keep the premium, and go back to step one.

That is the wheel. Sell puts, potentially get assigned, sell calls, potentially get called away, repeat. Each cycle you are collecting premium and reducing your effective cost basis on the position.

The part most people stop at.

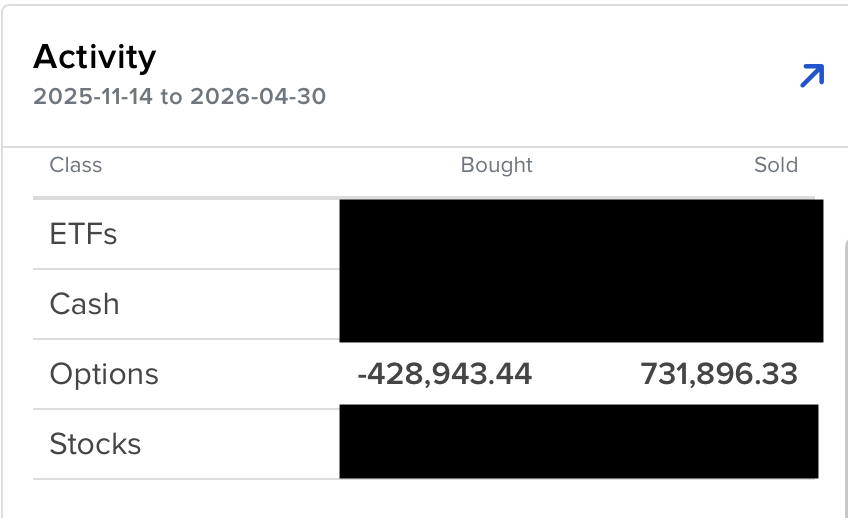

From November 2025 to April 2026, here is what my IBKR activity report shows.

IBKR activity report: Nov 2025 to Apr 2026

Gross options sold: $731,896. Gross options bought: $428,943. Net premium collected: roughly $302,000 over about five and a half months.

That is the number most people screenshot and post online. And I get it, it looks good. But if you stop there you are telling less than half the story.

The bought side is not just losses. It includes positions I closed early, rolls where I bought back one contract and sold another further out, and general position management. The net figure of $302k is what actually stayed in my pocket after all that activity.

What $302k in net premium does not tell you.

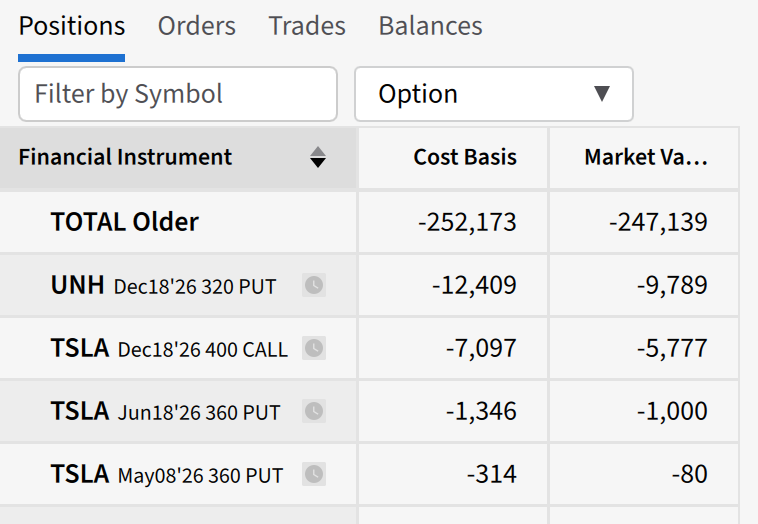

Here are my current open positions as of today.

Current open options positions on IBKR

I have about $252k in open option positions by cost basis. Current market value is around $247k. If I closed everything today I would pay roughly $247k to buy back those positions. That $5k difference is unrealised profit sitting in the open book.

Looking at the positions: TSLA calls at $400 strike expiring December 2026, TSLA puts at $360 expiring June and May 2026, and UNH puts at $320 expiring December 2026. Given where these are currently trading, most of these look set to expire out of the money. The May TSLA put has a market value of just $80 against a cost basis of $314, so that one is basically done.

Best case scenario: everything expires worthless, I pay nothing to close, and I keep the remaining $247k on top of the $302k already collected. Fat hope, but that is the ideal. Realistic trajectory looks okay though.

And even that best case does not show the complete picture, because there is another layer underneath all of this.

Assignments, stock positions, and why true P&L is hard to calculate.

When a put gets assigned, you do not just collect premium and move on. You actually buy the stock. That stock now has its own profit and loss depending on where the price goes from there. And if you are wheeling while also holding stocks for the long term, the two get tangled together in ways that are genuinely difficult to separate.

That is exactly my situation. I have been wheeling while building long-term stock positions, and some of my wheeling has led me to accumulate stock in companies that have since dropped significantly. LULU is one of them. Another holding I will keep nameless for now. It is a large enough bet that the outcome is essentially either a landed property or a modest retirement. Eyes open, calculated risk.

So why am I not more worried?

Because of wheeling.

Every round of premium I collected reduced my effective cost basis on those stock positions. I got into some of these at a lower real cost than the market price because I was paid to take the risk. When the price dropped, my actual loss was smaller than it looked on paper because the premium collected along the way was already cushioning it.

TSLA and UNH in particular have been consistent performers for me. Both sit in my top five tickers by return, and the premium from wheeling them has been meaningful. The wheel does not just generate income in isolation, it changes the economics of how you own a stock.

The honest conclusion I keep coming back to: I am better off having wheeled than not having wheeled. Even with the complicated stock positions, even with the concentrated bets, the premium collected has sheltered me from a much larger drawdown than I would have otherwise experienced.

Why I am building my own options tracker.

There is no clean off-the-shelf dashboard that shows you: premium collected, minus buyback costs, minus assignment losses, plus or minus unrealised stock P&L, equals your true wheel performance. At least not one that handles the nuance of mixing long-term stock holdings with active wheeling on the same positions.

This is why I am building my own tool. I want to see real cost basis per position including all premium received, realised versus unrealised P&L separated cleanly, and how each assignment has affected my overall exposure. The $302k net number is real. But it is a starting point for the analysis, not the conclusion.

Want to see what the wheel actually looks like in practice? Try the free TSLA wheel simulator I built. No login needed.

Try the free wheel simulatorThe honest take on the wheel strategy.

The wheel strategy works. It is not magic, it is not fully passive income, and it does not protect you from a stock going to zero. But if you are investing in stocks you believe in anyway, getting paid premium while you wait is a sensible approach.

For Singapore retail investors using platforms like IBKR, this is a legitimate income strategy that does not require you to be a full-time trader. You are selling options on stocks you already want to own, collecting premium each cycle, and systematically lowering your cost basis over time.

Just do not screenshot the gross number and call it done. The full picture is always more complicated, and anyone who tells you otherwise is selling something.